All Categories

Featured

Table of Contents

Policies can likewise last till specified ages, which in the majority of cases are 65. Beyond this surface-level details, having a better understanding of what these strategies involve will assist ensure you buy a plan that fulfills your needs.

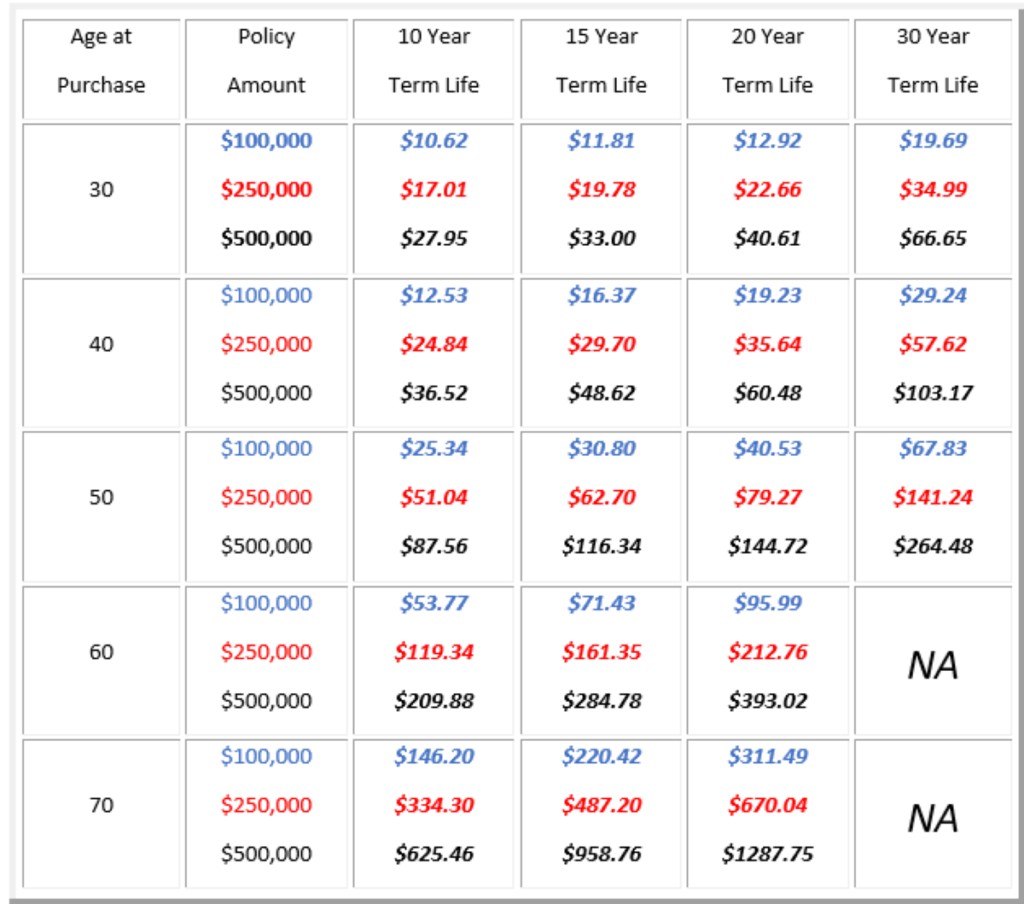

Be conscious that the term you choose will certainly affect the premiums you spend for the policy. A 10-year level term life insurance policy plan will certainly cost less than a 30-year plan due to the fact that there's much less possibility of a case while the strategy is active. Reduced threat for the insurer equates to decrease premiums for the insurance policy holder.

Your family's age must also influence your policy term choice. If you have kids, a longer term makes good sense due to the fact that it shields them for a longer time. Nonetheless, if your kids are near their adult years and will certainly be financially independent in the close to future, a shorter term may be a much better suitable for you than a prolonged one.

Nonetheless, when contrasting whole life insurance policy vs. term life insurance, it's worth keeping in mind that the latter commonly sets you back less than the previous. The outcome is more insurance coverage with reduced premiums, providing the finest of both worlds if you need a considerable quantity of coverage however can not manage an extra costly plan.

How Does Term Life Insurance Work for Families?

A degree death benefit for a term policy usually pays as a lump amount. When that happens, your successors will get the entire quantity in a single payment, and that amount is ruled out revenue by the IRS. Those life insurance proceeds aren't taxable. Nonetheless, some level term life insurance policy firms permit fixed-period repayments.

Rate of interest repayments obtained from life insurance coverage policies are considered revenue and go through tax. When your level term life plan runs out, a few different points can take place. Some insurance coverage terminates immediately without any option for revival. In various other circumstances, you can pay to expand the strategy beyond its initial day or transform it into a permanent policy.

The disadvantage is that your renewable degree term life insurance policy will feature higher premiums after its preliminary expiry. Advertisements by Money. We may be compensated if you click this ad. Advertisement For newbies, life insurance can be made complex and you'll have inquiries you want responded to prior to committing to any kind of policy.

Life insurance business have a formula for calculating danger making use of death and rate of interest (Term Life Insurance). Insurance firms have countless clients obtaining term life plans at the same time and use the costs from its energetic plans to pay enduring beneficiaries of various other policies. These business use mortality to approximate the number of people within a specific group will certainly file death cases annually, and that details is utilized to identify ordinary life expectancies for potential policyholders

In addition, insurance coverage companies can spend the cash they obtain from premiums and increase their income. The insurance company can spend the cash and earn returns.

The following section details the advantages and disadvantages of level term life insurance policy. Predictable premiums and life insurance policy protection Streamlined policy framework Potential for conversion to long-term life insurance policy Minimal insurance coverage duration No cash money worth build-up Life insurance coverage premiums can enhance after the term You'll locate clear benefits when comparing degree term life insurance policy to other insurance coverage types.

Key Features of Term Life Insurance For Couples Explained

You always understand what to expect with affordable level term life insurance policy coverage. From the minute you take out a plan, your premiums will never alter, aiding you plan monetarily. Your insurance coverage won't differ either, making these policies reliable for estate planning. If you value predictability of your payments and the payouts your heirs will receive, this sort of insurance policy can be a great fit for you.

If you go this path, your costs will certainly boost yet it's always great to have some adaptability if you want to maintain an active life insurance coverage plan. Sustainable degree term life insurance policy is one more choice worth taking into consideration. These plans permit you to keep your existing strategy after expiration, supplying versatility in the future.

What is 30-year Level Term Life Insurance? A Simple Explanation?

You'll pick a protection term with the finest degree term life insurance coverage prices, but you'll no much longer have protection once the strategy ends. This drawback could leave you clambering to locate a new life insurance coverage policy in your later years, or paying a premium to prolong your existing one.

Several whole, global and variable life insurance policy plans have a cash money value component. With among those plans, the insurance provider transfers a part of your month-to-month costs repayments into a cash money worth account. This account gains rate of interest or is invested, assisting it expand and supply an extra substantial payment for your beneficiaries.

With a level term life insurance policy plan, this is not the instance as there is no money worth component. Therefore, your policy won't grow, and your death advantage will certainly never increase, thus restricting the payment your beneficiaries will certainly obtain. If you desire a plan that gives a survivor benefit and builds cash money value, check out whole, universal or variable strategies.

The 2nd your plan expires, you'll no more live insurance coverage. It's often feasible to renew your policy, however you'll likely see your premiums boost dramatically. This could provide issues for retirees on a fixed income due to the fact that it's an additional cost they might not have the ability to manage. Level term and lowering life insurance coverage deal comparable policies, with the major difference being the fatality benefit.

It's a sort of cover you have for a specific quantity of time, referred to as term life insurance policy. If you were to die while you're covered for (the term), your loved ones get a fixed payment concurred when you obtain the policy. You just select the term and the cover quantity which you might base, as an example, on the expense of raising youngsters until they leave home and you might make use of the payment towards: Assisting to pay off your home loan, financial debts, bank card or lendings Assisting to pay for your funeral costs Assisting to pay university fees or wedding costs for your kids Aiding to pay living prices, replacing your revenue.

What is Level Term Vs Decreasing Term Life Insurance and Why Is It Important?

The policy has no money worth so if your settlements stop, so does your cover. The payout remains the exact same throughout the term. If you take out a level term life insurance plan you might: Choose a taken care of quantity of 250,000 over a 25-year term. If throughout this time around you pass away, the payment of 250,000 will be made.

{kind=link}

Latest Posts

Funeral Insurance For Over 65

Global Burial Insurance

Life Insurance Quotes Online Instant