All Categories

Featured

Table of Contents

Many entire, universal and variable life insurance plans have a cash value component. With among those policies, the insurance firm deposits a portion of your regular monthly premium repayments into a money worth account. This account earns rate of interest or is invested, helping it grow and offer an extra substantial payment for your recipients.

With a degree term life insurance coverage plan, this is not the instance as there is no money value element. Therefore, your plan won't grow, and your death advantage will never ever increase, therefore limiting the payment your beneficiaries will certainly obtain. If you want a policy that offers a survivor benefit and constructs money worth, explore entire, universal or variable strategies.

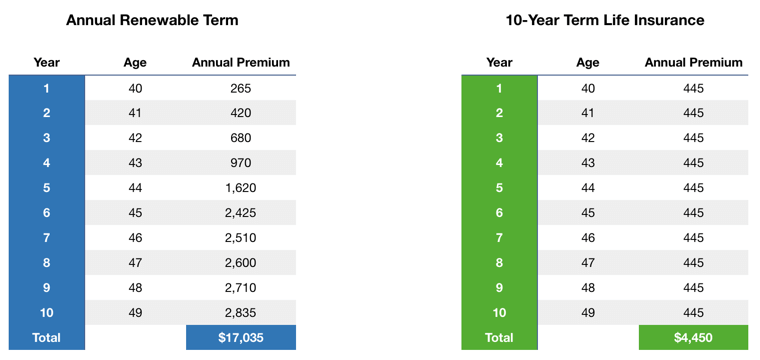

The second your plan ends, you'll no much longer live insurance coverage. It's frequently possible to renew your policy, but you'll likely see your premiums raise dramatically. This might offer problems for retirees on a fixed revenue since it's an additional cost they could not have the ability to afford. Level term and decreasing life insurance policy offer comparable policies, with the main difference being the survivor benefit.

(EST).2. On the internet applications for the are available on the on the AMBA website; click the "Apply Now" blue box on the right-hand man side of the web page. NYSUT participants can additionally print out an application if they would prefer by clicking the on the AMBA internet site; you will then require to click "Application" under "Forms" on the right-hand man side of the page.

Where can I find Level Term Life Insurance For Young Adults?

NYSUT members registered in our Level Term Life Insurance Policy Strategy have access to given at no added expense. The NYSUT Member Advantages Trust-endorsed Degree Term Life Insurance coverage Strategy is underwritten by Metropolitan Life Insurance Business and administered by Association Member Conveniences Advisors. NYSUT Student Members are not eligible to take part in this program.

Term life insurance policy is a cost effective and uncomplicated option for lots of people. You pay premiums monthly and the coverage lasts for the term length, which can be 10, 15, 20, 25 or thirty years. What takes place to your costs as you age depends on the kind of term life insurance policy coverage you buy.

As long as you continue to pay your insurance policy premiums each month, you'll pay the same price during the entire term length which, for lots of term policies, is commonly 10, 15, 20, 25 or 30 years (Level term life insurance companies). When the term finishes, you can either choose to end your life insurance policy coverage or restore your life insurance policy plan, typically at a greater rate

Who has the best customer service for Compare Level Term Life Insurance?

For instance, a 35-year-old woman in outstanding health and wellness can get a 30-year, $500,000 Sanctuary Term plan, issued by MassMutual starting at $29.15 each month. Over the next 30 years, while the policy remains in location, the price of the protection will certainly not transform over the term period. Allow's face it, most of us don't such as for our costs to expand in time.

Your degree term rate is established by a number of variables, many of which are relevant to your age and health and wellness. Other elements include your details term policy, insurance coverage company, benefit amount or payment. Throughout the life insurance policy application procedure, you'll address questions regarding your health background, including any pre-existing conditions like a critical ailment.

It's always very crucial to be honest in the application procedure. Issuing the policy and paying its advantages relies on the candidate's evidence of insurability which is figured out by your response to the health inquiries in the application. A medically underwritten term plan can secure in an economical price for your protection duration, whether that be 10, 15, 20, 25 or thirty years, no matter of how your wellness could transform throughout that time.

With this sort of degree term insurance coverage policy, you pay the same monthly premium, and your beneficiary or recipients would certainly get the same benefit in the event of your fatality, for the entire coverage period of the policy. So exactly how does life insurance policy work in terms of price? The cost of level term life insurance will certainly depend upon your age and health along with the term length and insurance coverage amount you select.

What should I know before getting 20-year Level Term Life Insurance?

Life: AgeGenderFace AmountTerm LengthPremium30Male$500,00030$29.9930 Women$1,000,00030$43.3135 Male$500,00020$20.7235 Women$750,00020$23.1340 Male$600,00015$22.8440 Women$800,00015$27.72 Price quote based upon prices for eligible Place Simple applicants in outstanding health and wellness. Pricing differences will certainly differ based upon ages, health condition, insurance coverage amount and term length. Haven Simple is currently not offered in DE, ND, NY, and SD.Regardless of what coverage you pick, what the policy's cash worth is, or what the swelling sum of the survivor benefit becomes, comfort is amongst one of the most valuable benefits connected with purchasing a life insurance plan.

Why would certainly someone pick a policy with an annually eco-friendly costs? It may be an alternative to think about for someone that needs protection only momentarily. For instance, an individual that is between jobs however desires survivor benefit security in location due to the fact that she or he has financial obligation or other financial commitments might wish to take into consideration an each year sustainable policy or something to hold them over until they begin a brand-new work that uses life insurance - Level term life insurance protection.

You can normally restore the policy every year which provides you time to consider your options if you desire insurance coverage for longer. Realize that those alternatives will involve paying more than you used to. As you grow older, life insurance premiums come to be significantly more costly. That's why it's helpful to acquire the appropriate amount and length of coverage when you initially obtain life insurance coverage, so you can have a low price while you're young and healthy.

If you contribute vital overdue labor to the household, such as childcare, ask on your own what it could set you back to cover that caretaking job if you were no more there. Then, see to it you have that insurance coverage in position to make sure that your household obtains the life insurance policy benefit that they need.

How long does Level Term Life Insurance Quotes coverage last?

For that set amount of time, as long as you pay your premium, your rate is steady and your recipients are secured. Does that imply you should always select a 30-year term size? Not always. In general, a shorter term plan has a reduced premium rate than a much longer plan, so it's clever to choose a term based upon the forecasted size of your monetary obligations.

These are very important aspects to remember if you were assuming concerning choosing a permanent life insurance policy such as an entire life insurance policy policy. Many life insurance policy plans provide you the option to add life insurance coverage cyclists, assume added benefits, to your policy. Some life insurance policy policies include cyclists built-in to the cost of premium, or motorcyclists might be available at a price, or have fees when exercised.

With term life insurance coverage, the interaction that most individuals have with their life insurance policy business is a monthly expense for 10 to 30 years. You pay your month-to-month premiums and wish your family members will never ever need to utilize it. For the group at Sanctuary Life, that appeared like a missed possibility.

{kind=link}

Latest Posts

Funeral Insurance For Over 65

Global Burial Insurance

Life Insurance Quotes Online Instant