All Categories

Featured

Table of Contents

Insurance provider will not pay a small. Instead, take into consideration leaving the cash to an estate or trust fund. For even more comprehensive information on life insurance policy obtain a duplicate of the NAIC Life Insurance Buyers Guide.

The IRS places a restriction on just how much money can enter into life insurance policy costs for the policy and how rapidly such costs can be paid in order for the plan to maintain all of its tax obligation benefits. If specific limitations are exceeded, a MEC results. MEC insurance holders might be subject to taxes on circulations on an income-first basis, that is, to the level there is gain in their policies, along with fines on any kind of taxed quantity if they are not age 59 1/2 or older.

Please note that impressive loans accumulate rate of interest. Earnings tax-free treatment likewise thinks the financing will eventually be pleased from revenue tax-free survivor benefit proceeds. Lendings and withdrawals minimize the policy's cash value and death benefit, may trigger specific policy benefits or bikers to come to be not available and may raise the chance the plan may lapse.

A customer might certify for the life insurance policy, however not the motorcyclist. A variable global life insurance contract is an agreement with the primary function of offering a death advantage.

Who are the cheapest Guaranteed Benefits providers?

These portfolios are very closely managed in order to satisfy stated investment objectives. There are fees and costs associated with variable life insurance policy contracts, consisting of mortality and risk fees, a front-end tons, administrative fees, financial investment monitoring fees, surrender costs and fees for optional riders. Equitable Financial and its affiliates do not offer lawful or tax advice.

Whether you're starting a family or marrying, people typically start to think of life insurance policy when someone else begins to depend upon their capacity to gain an earnings. Which's fantastic, because that's exactly what the survivor benefit is for. But, as you discover more about life insurance policy, you're likely to locate that numerous plans for example, whole life insurance policy have greater than simply a fatality benefit.

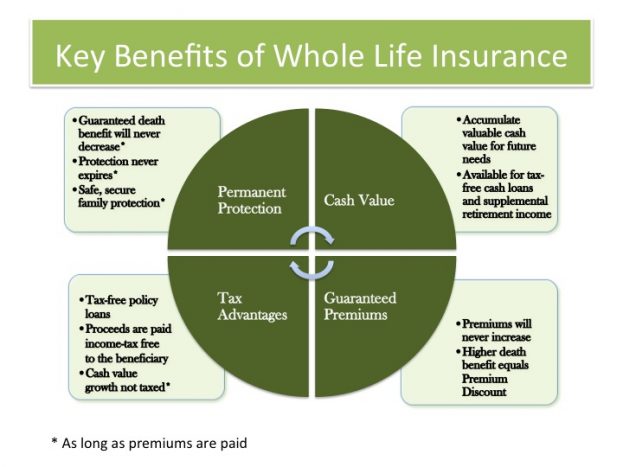

What are the benefits of whole life insurance coverage? One of the most attractive benefits of acquiring a whole life insurance coverage plan is this: As long as you pay your costs, your death benefit will certainly never ever run out.

Believe you don't need life insurance policy if you do not have youngsters? You might intend to believe again. It may appear like an unnecessary cost. Yet there are many advantages to having life insurance, also if you're not supporting a family. Here are 5 reasons that you must purchase life insurance policy.

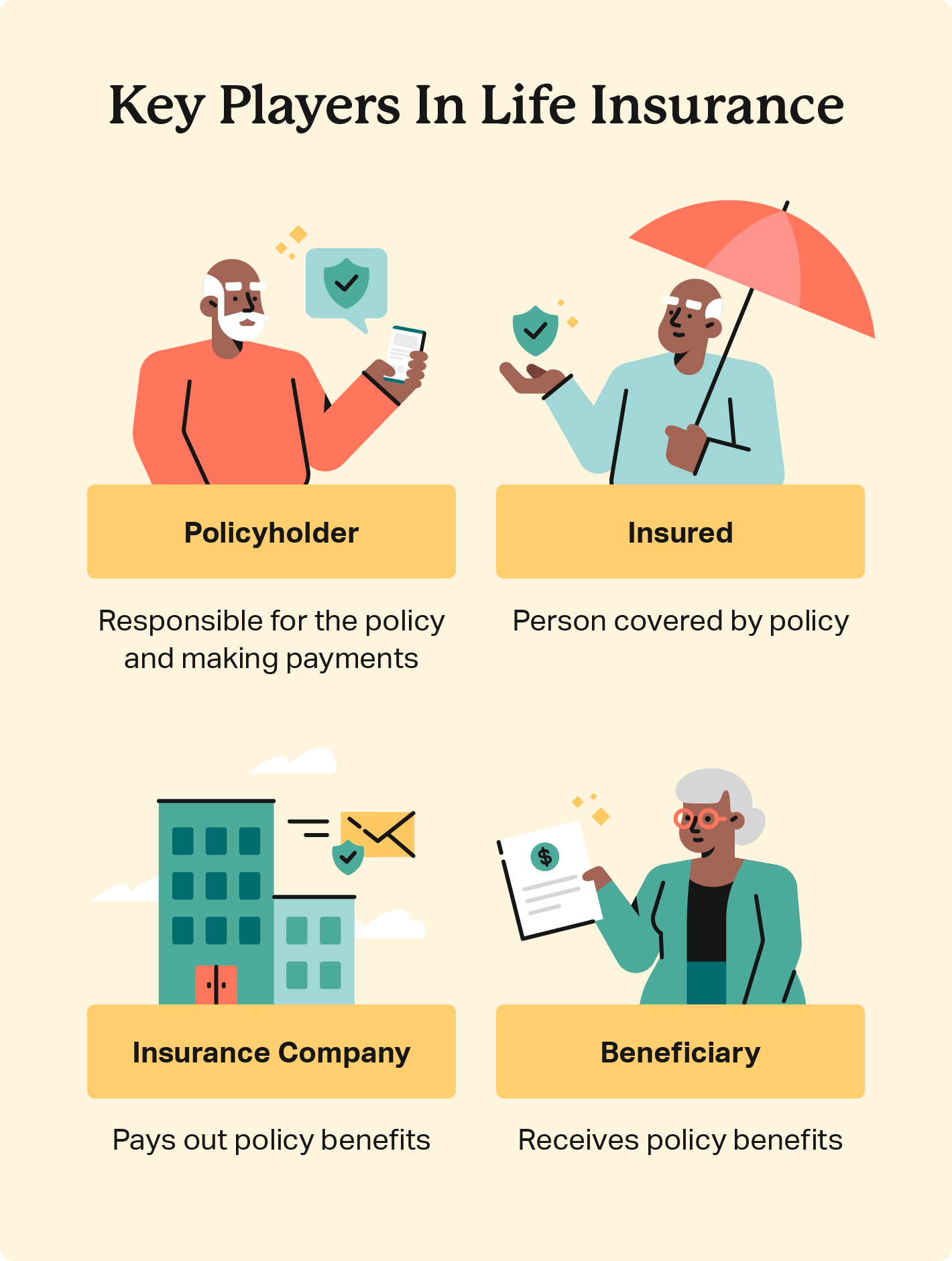

Beneficiaries

Funeral costs, funeral prices and medical expenses can accumulate (Family protection). The last point you want is for your loved ones to bear this extra problem. Permanent life insurance policy is available in numerous amounts, so you can select a fatality benefit that satisfies your requirements. Alright, this just uses if you have kids.

Determine whether term or long-term life insurance policy is ideal for you. Get a price quote of exactly how much insurance coverage you might require, and just how much it can set you back. Discover the correct amount for your budget plan and peace of mind. Locate your amount. As your personal situations adjustment (i.e., marital relationship, birth of a kid or job promotion), so will certainly your life insurance policy requires.

Essentially, there are 2 kinds of life insurance intends - either term or long-term plans or some mix of the two. Life insurance companies use various kinds of term strategies and traditional life plans as well as "rate of interest sensitive" items which have actually come to be more widespread since the 1980's.

Term insurance gives security for a specified time period. This duration can be as brief as one year or supply coverage for a details number of years such as 5, 10, two decades or to a defined age such as 80 or in many cases as much as the oldest age in the life insurance policy mortality tables.

What are the benefits of Protection Plans?

Presently term insurance prices are very competitive and among the lowest historically knowledgeable. It must be noted that it is a commonly held belief that term insurance policy is the least pricey pure life insurance coverage readily available. One needs to examine the plan terms very carefully to decide which term life options are ideal to fulfill your specific conditions.

With each new term the premium is increased. The right to restore the policy without evidence of insurability is an essential advantage to you. Or else, the threat you take is that your health might deteriorate and you might be not able to acquire a plan at the same prices and even in all, leaving you and your recipients without coverage.

You must exercise this option throughout the conversion duration. The size of the conversion duration will certainly vary depending upon the sort of term policy acquired. If you transform within the prescribed duration, you are not called for to provide any info about your health and wellness. The premium rate you pay on conversion is usually based on your "present obtained age", which is your age on the conversion day.

Under a degree term plan the face amount of the plan continues to be the very same for the whole period. With reducing term the face amount lowers over the period. The premium stays the same each year. Frequently such plans are offered as mortgage defense with the quantity of insurance reducing as the balance of the mortgage lowers.

Is there a budget-friendly Term Life option?

Typically, insurance firms have not had the right to alter premiums after the plan is marketed. Considering that such policies may proceed for years, insurance providers should make use of traditional mortality, passion and expenditure price price quotes in the costs estimation. Adjustable premium insurance policy, however, enables insurance firms to provide insurance policy at reduced "present" costs based upon much less conventional presumptions with the right to transform these costs in the future.

While term insurance policy is developed to provide defense for a defined time period, long-term insurance policy is developed to provide protection for your entire lifetime. To keep the premium rate level, the costs at the more youthful ages goes beyond the real cost of protection. This additional premium develops a get (cash value) which assists spend for the policy in later years as the price of protection rises over the premium.

Under some policies, costs are called for to be paid for a set number of years. Under other plans, costs are paid throughout the insurance policy holder's life time. The insurer spends the excess premium dollars This type of plan, which is occasionally called cash money value life insurance policy, generates a cost savings component. Cash worths are vital to an irreversible life insurance plan.

{kind=link}

Latest Posts

Funeral Insurance For Over 65

Global Burial Insurance

Life Insurance Quotes Online Instant